This month’s real estate investing update is all about movement — from rate cuts and market shifts to our own WCP brand evolution.

If you’ve been following the news, you’ve seen the Fed’s September rate cut make waves across every financial headline. But for investors? The story runs deeper — because the Fed doesn’t actually control mortgage rates.

Let’s unpack what’s really driving the market, and what it means for your next investment strategy.

When the Fed changes rates, most people expect mortgage rates to follow. But that’s not how it works.

The Federal Funds Rate only impacts short-term lending — think credit cards, business lines, and HELOCs. Mortgage rates, however, follow the 10-year Treasury yield, which reflects how institutional investors (banks, pension funds, and governments) feel about inflation and economic growth.

The real number to watch? The 10-year Treasury, not Jerome Powell’s podium.

When investors expect strong growth or inflation, they sell bonds — yields rise, and so do mortgage rates. When they expect weakness or uncertainty, they buy bonds — yields fall, and mortgage rates follow.

So while the Fed can sway sentiment, it doesn’t pull the strings. The bond market does.

For fix-and-flip investors and rental property owners, the recent rate cut might feel like a step forward — but your borrowing costs depend more on bond yields than central bank policy.

If the 10-year yield drifts lower, you could see gradual improvements in DSCR rental loan and fix-and-flip financing — not an overnight drop. Flippers might benefit as more buyers re-enter the market, helping move finished inventory faster.

Until yields decline significantly, capital costs and holding expenses will stay high. That means it’s time to play smart and stay strategic.

Investor Takeaways:

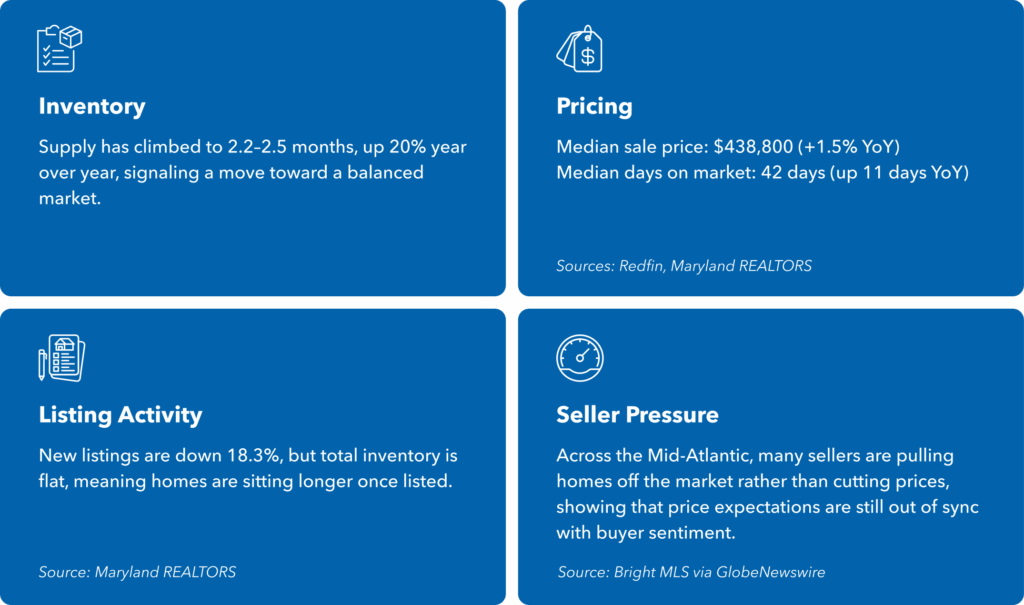

This fall market is full of mixed signals: lower Fed rates, stubborn borrowing costs, and gradually improving inventory.

For Maryland investors, that means:

Buy smart: More supply = better negotiating room.

Sell strategically: Overpricing kills momentum.

Watch the 10-year yield: It reveals more about your financing future than the Fed ever will. The Fed may grab the headlines — but the bond market still writes the script