After years of rate shock, frozen inventory, and margin pressure, the DMV housing market is entering 2026 in a far more investor friendly position.

This is not a boom. It is not a bust. It is a reset to normalcy. And resets tend to create opportunities for disciplined capital.

Below is a clear-eyed look at what is actually happening across inventory, rates, pricing, and investor strategy in the DC, Maryland, and Virginia market.

For most of the past three years, inventory was artificially suppressed by homeowners locked into 2–3% mortgages. That dynamic is beginning to ease.

What we are seeing:

Deal flow is improving, especially for value-add and distress-adjacent assets.

Mortgage rates are no longer rising, and that alone is changing market behavior.

Where rates stand:

Rates are not cheap, but they are predictable. And predictability is what capital needs.

The headline fear going into 2025 was a major correction. That never materialized, but price growth did stall.

Current reality:

This is a compression phase, not a collapse.

What this creates:

For long-term holders, this is a healthy pause.

For flippers, underwriting discipline matters more than ever.

The DMV market is no longer dominated by:

Instead, we’re entering a balanced, transaction-driven market, where fundamentals matter again.

That favors:

Markets like this reward preparation, not speculation.

2026 isn’t about chasing appreciation.

It’s about buying right, structuring smart debt, and letting your skills do the rest.

For investors actively sourcing deals in DC, Maryland, or Virginia, this is the most rational market we have seen in years.

And rational markets are where professionals win.

Let’s Talk About Your Next Funding →

This month’s real estate investing update is all about movement — from rate cuts and market shifts to our own WCP brand evolution.

If you’ve been following the news, you’ve seen the Fed’s September rate cut make waves across every financial headline. But for investors? The story runs deeper — because the Fed doesn’t actually control mortgage rates.

Let’s unpack what’s really driving the market, and what it means for your next investment strategy.

When the Fed changes rates, most people expect mortgage rates to follow. But that’s not how it works.

The Federal Funds Rate only impacts short-term lending — think credit cards, business lines, and HELOCs. Mortgage rates, however, follow the 10-year Treasury yield, which reflects how institutional investors (banks, pension funds, and governments) feel about inflation and economic growth.

The real number to watch? The 10-year Treasury, not Jerome Powell’s podium.

When investors expect strong growth or inflation, they sell bonds — yields rise, and so do mortgage rates. When they expect weakness or uncertainty, they buy bonds — yields fall, and mortgage rates follow.

So while the Fed can sway sentiment, it doesn’t pull the strings. The bond market does.

For fix-and-flip investors and rental property owners, the recent rate cut might feel like a step forward — but your borrowing costs depend more on bond yields than central bank policy.

If the 10-year yield drifts lower, you could see gradual improvements in DSCR rental loan and fix-and-flip financing — not an overnight drop. Flippers might benefit as more buyers re-enter the market, helping move finished inventory faster.

Until yields decline significantly, capital costs and holding expenses will stay high. That means it’s time to play smart and stay strategic.

Investor Takeaways:

This fall market is full of mixed signals: lower Fed rates, stubborn borrowing costs, and gradually improving inventory.

For Maryland investors, that means:

Buy smart: More supply = better negotiating room.

Sell strategically: Overpricing kills momentum.

Watch the 10-year yield: It reveals more about your financing future than the Fed ever will. The Fed may grab the headlines — but the bond market still writes the script

Let’s Talk About Your Next Funding →

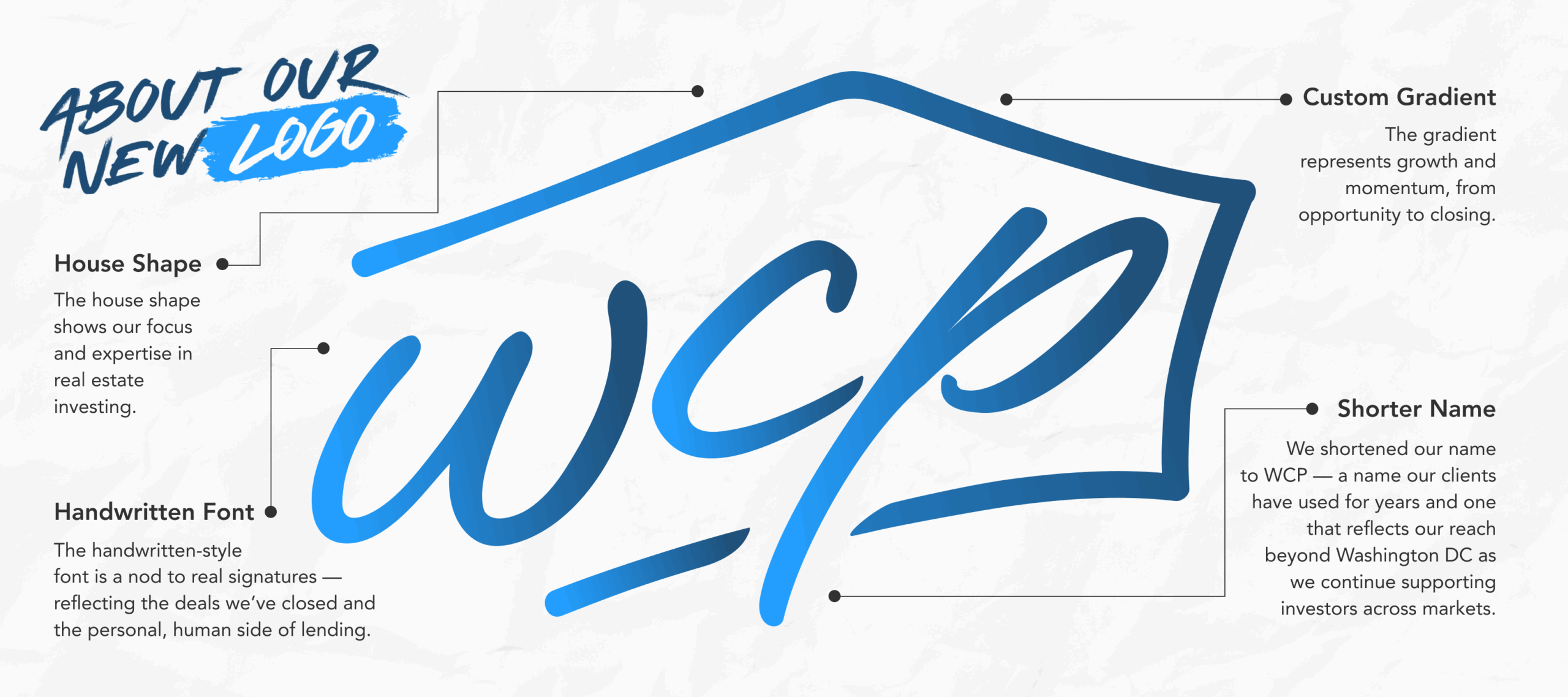

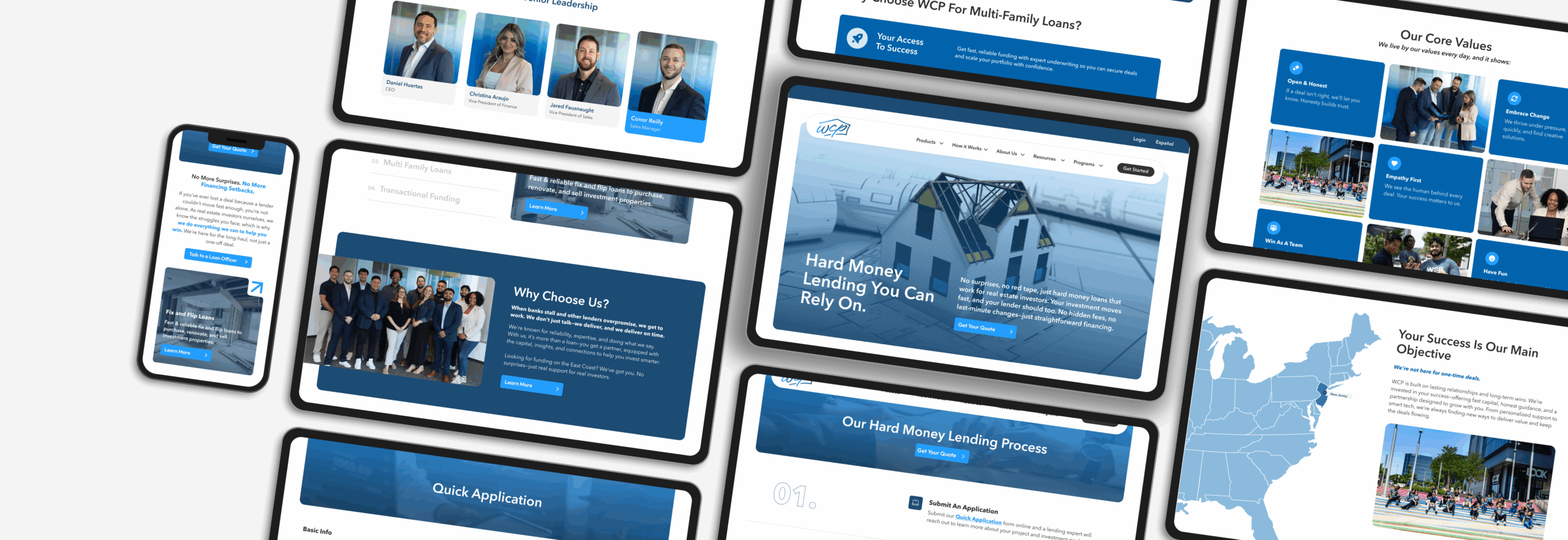

We are proud to announce the launch of our new brand and website, designed with real estate investors and lending partners in mind.

As one of the most trusted hard money lenders in the region, we’ve grown steadily over the years. It was time for our brand to reflect that growth and the level of service we’re known for.

“Since day one, we’ve been focused on giving real estate investors the tools and support they need to succeed. This rebrand is about reflecting how far we’ve come and how committed we are to where our clients are headed.” —Daniel Huertas, Founder and CEO

From fix and flip loans to long-term real estate funding solutions, everything we do is built around your goals.

While our look has evolved, our commitment remains the same. We are still the private lending team you know and trust, now with a sharper and more aligned foundation.

This isn’t a reinvention. It is a realignment with the way real estate investors do business today.

Our new logo is more than just a design update. It’s a reflection of who we are and how we support investors like you.

The new WCP site was built with our clients in mind. It’s faster, easier to use, and structured around the way real estate investors actually do business.

Whether you are applying for fix and flip loans, looking for rental property financing, or checking out new investment opportunities, the new site delivers a streamlined experience that reflects how today’s investors operate.

We have always believed that financial freedom through real estate should be accessible, achievable, and transparent. Now we are putting that message front and center.

To make financial freedom accessible and achievable for all by equipping investors with the resources they need through transparency, expertise, and reliable, personalized support.

We see every deal as a relationship, not a transaction. When you partner with WCP, you get a team that genuinely cares about your goals and works hard to help you achieve them.

We believe in doing what we say. Our clients rely on us to deliver with clarity, consistency, and follow-through — and we take that seriously.

Our rebrand is built on four core pillars. These are not just brand statements. They are the lens through which we operate every day.

With decades of experience in real estate and lending, we provide investors with real-world insights and tools to move with confidence, even when the market shifts.

Every investor is different. That’s why we personalize each deal to fit your strategy, not the other way around.

To better reflect who we are today. Our new look and messaging not only match the high standard of service our clients already know us for, but also marks our expansion beyond DC to serve real estate investors nationwide.

Not at all. You will still be working with the same WCP team.

No. Our programs remain the same. The way we present and support them is now even clearer.

There is nothing you need to do. Your deals, contacts, and borrower portal access are all the same. The only difference is a smoother, more aligned experience.

Yes, your existing loan terms and payment details remain exactly the same. If you have any questions or just want to talk through the rebrand, reach out to your loan officer anytime. We’re always here to help.

This rebrand is about delivering an experience that reflects the values we’ve always stood for. We are still the same team, with the same commitment to helping you succeed. Now, we are just doing it with a sharper focus and a clearer message

We are glad you are here for the next chapter.

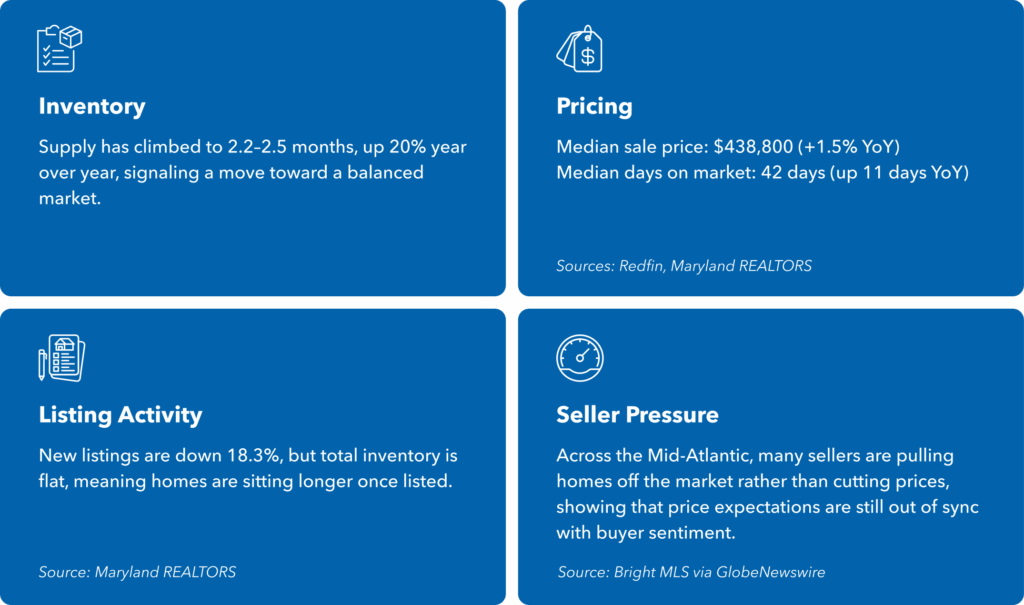

August data shows the DMV real estate market is slowing down and inching closer to balance. Sellers still have some leverage, but buyers are gaining ground — and that shift carries big implications for real estate investors on both sides of a deal.

At Washington Capital Partners (WCP), we’ve seen this before. These moments of transition often create the biggest opportunities for investors who know how to play both sides.

Months of Supply: Inventory has climbed to nearly two months of supply. It’s not a buyer’s market yet, but this is the highest level since 2020.

Stale Listings: Roughly one in five homes has been on the market for over 90 days without a sale.

Price Cuts: More sellers are missing their mark, with a growing share of homes selling below list price compared to 2024.

Withdrawn Listings: Thousands of properties have been removed from the market after failing to attract offers.

Together, these signals point to a market softening that savvy real estate investors can use to their advantage.

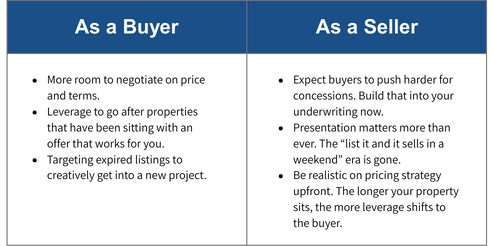

We’re moving out of the pure seller’s market of the past few years and into a more balanced playing field. That means:

Remember: your first offer is often your best offer. Waiting for something “better” can backfire and lead to price cuts or extended carrying costs that eat into profits.

Inventory is climbing, buyers have more choices, and sellers who don’t adjust will get stuck.

For investors, that creates opportunity—especially if you’re prepared with reliable, fast funding and a lender who keeps their word.

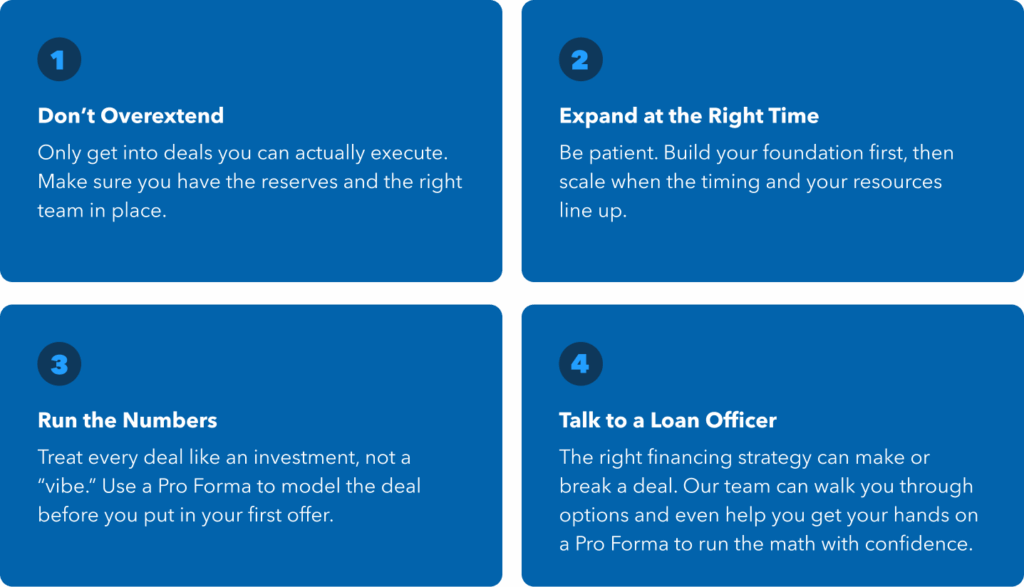

One of the biggest mistakes new investors make is trying to take on too many deals at once. Growth is exciting, but in real estate investing, moving too fast can lead to costly mistakes.

Start small. Focus on low-risk cosmetic updates, build confidence, and grow from there. The key is to start—and to make sure every deal is structured with the right financing behind it.

A pro forma is a financial projection that shows how an investment property is expected to perform. Think of it as a forward-looking budget: instead of recording what has already happened, it models what’s likely to happen based on your assumptions.

For fix and flip projects and DSCR rental investments alike, a solid pro forma helps you identify risk, project returns, and secure the best lending terms.

Talk To A Loan Officer Today! →

If you’re investing in the DMV area, you’ve likely heard about the recent fraud scandal that’s rocked the real estate investing world and disrupted the DSCR loan market.

A group of investors, appraisers, an appraisal management company (AMC), and possibly a title company orchestrated a scheme to inflate property values and secure DSCR loans under false pretenses.

The fraud impacted an estimated 500–800 loans totaling between $200–300 million. Most of the activity occurred in Baltimore, with additional cases suspected in parts of New Jersey and Brooklyn, NY.

The scheme worked like this:

The scam unraveled when an Apollo-backed firm noticed multiple appraisal invoices for exactly $444 — all tied to the same appraisers and sponsors. That discovery triggered a wider investigation, and the full repercussions are expected to unfold in the months ahead.

Some lenders have already paused lending in Baltimore as a result of the fraud fallout.

But WCP is still lending — both fix and flip and DSCR — in Baltimore City.

That said, investors should expect more scrutiny on:

If you’re investing in Baltimore, keep an eye out for a potential surge in auction properties. Many of these distressed assets are likely connected to this scheme — which could temporarily impact comps and put downward pressure on nearby property values.

Still, these same conditions may create strong opportunities for informed investors ready to buy carefully and leverage transparent, trustworthy private lending.

Talk to Washington Capital Partners about your Baltimore deals before you make your next move.

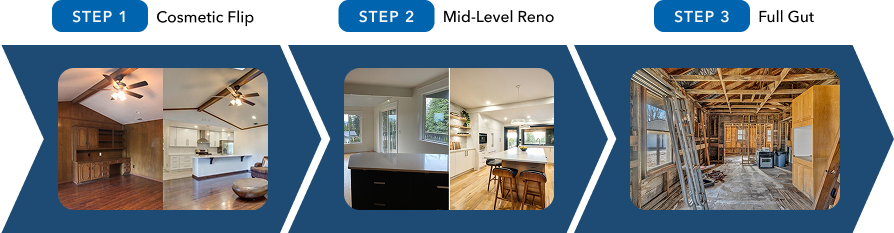

You don’t need deep pockets to start investing in real estate. Many successful investors begin with simple “lipstick” renovations — paint, floors, and basic cosmetic updates that quickly add value without the cost or risk of a full renovation.

Start small. Focus on low-risk cosmetic updates, build confidence, and grow from there. The key is to start.

When you’re selecting your first investment property:

Pro tip: Your first flip doesn’t have to be your dream flip. It just has to get you in the game.

A fresh twist is unfolding in the DMV real estate market — not just more listings, but a change in who’s selling.

In Washington, DC, roughly 15% of spring home sales came from retirees, compared to the usual under-10% across the mid-Atlantic. This rise is driven largely by federal workforce reductions prompting early retirements — and it’s creating new openings for real estate investors ready to move fast.

These aren’t distressed sellers. They’re long-time homeowners with 30–40 years of equity, ready to cash out.

What these sellers want:

That’s your edge.

These aren’t 2022-style flipper trades. They’re off-market or estate-condition homes with serious upside — if you move fast and tailor terms to the seller.

The best opportunities won’t come from comps. They’ll come from recognizing when life events are driving inventory. For savvy real estate investors in the DMV, this wave of retiree-driven listings represents a new kind of opportunity: stable properties with strong fundamentals and flexible sellers.

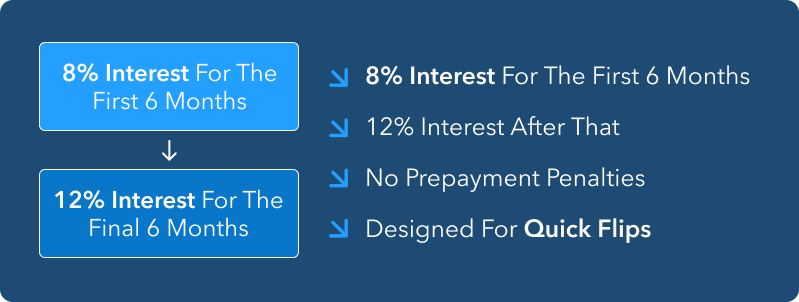

Looking for a smarter way to fund your next real estate investment? Qualified borrowers can access 8% interest for the first six months on a 12-month term, adjusting to 12% for the remaining six months.

If you’re planning your next fix and flip, this is the moment to lock in competitive rates from a private lender who moves fast and delivers on their word.

The best loan officers do more than just fund your project — they help you spot your next opportunity.

They will:

Pro Tip: A great loan officer doesn’t just back your deal. They help you find the next one.

Talk To Us About Finding Your Next Deal →

Flipping in the DMV is still profitable, but in 2025, margins are tighter. Real estate investors are being squeezed on three fronts: longer Days on Market (DOM), rising inventory, and softer prices.

Even experienced fix and flip investors are seeing that it’s not just about finding deals anymore — it’s about knowing how to buy, design, and price strategically to protect your upside.

| Longer Days on Market = Higher Holding Costs | Rising Inventory = More Competition | Flat or Falling Prices = Compressed ARVs |

|---|---|---|

| DC flips are averaging 54–90+ DOM | Inventory is up 56% year-over-year in DC | Some DC prices are flat or declining |

| Higher holding costs from interest, taxes, insurance, and staging | Buyers have more options and are taking longer to decide | Modest appreciation in parts of Maryland isn’t covering higher costs |

| Many investors are cutting prices or offering buyer incentives | Flips that don’t stand out or are overpriced get overlooked | Buyers are rate-sensitive and hesitant to pay premium prices |

| What to do: Be more selective when buying to protect your upside | What to do: Deliver standout value or come ready with incentives | What to do: Price accurately based on your micro-market |

The DMV market in 2025 looks different from the 2022 peak. Homes are taking longer to sell, competition among investors is tighter, and pricing strategy matters more than ever.

| 2022 | 2025 |

|---|---|

| Loose ARV projections in DMV real estate flips | Tight underwriting standards in real estate investing |

| “Test the ceiling” pricing on investment properties | Fast, focused execution on fix and flip projects |

| Overdesigned renovations focused on style, not ROI | Disciplined resale strategies to protect profit margins |

The best investors are adapting — refining acquisition strategies, tightening budgets, and partnering with reliable private lenders who understand the local market.

Even a great renovation can fall flat if the design choices don’t match the market. Here are three common missteps — and how to fix them.

Design choices that clash with the home’s architecture or local comps can hold your flip back.

How to Fix It: Match your finishes to what’s trending in your target buyer market. Keep color palettes neutral and consistent.

Sloppy landscaping or mismatched exterior details can turn buyers away before they step inside.

How to Fix It: Focus on landscaping, exterior paint, and updated entryways. A clean first impression builds trust.

Overly personalized finishes or gaudy lighting choices distract from the home’s value.

How to Fix It: Choose timeless, high-quality fixtures that appeal to the majority of buyers.

At Washington Capital Partners, we’re helping investors stay competitive with lending options built for today’s market realities.

Whether you need fix and flip loans to keep projects moving or bridge financing to manage longer hold times, WCP delivers the speed, transparency, and flexibility real estate investors depend on.

Talk to a Loan Officer Today →

While home prices remain high, appreciation has cooled compared to previous years. Some markets like New York City, parts of Connecticut, and Richmond are still seeing strong gains, but others are beginning to stabilize.

More listings are popping up, especially in higher price ranges. However, homes priced under $700K remain highly competitive across much of the DMV real estate market. Buyers in that range continue to face bidding wars and limited inventory, particularly in desirable neighborhoods with strong school districts and convenient access to major job centers.

Still Competitive: D.C. Metro, Northern Virginia, and Philadelphia suburbs.

Softening: Rural areas in Florida and parts of West Virginia, where buyers are gaining more negotiating power and sellers are starting to adjust pricing expectations.

In fast-moving markets, homes are selling in under 30 days. In slower regions, listings can sit for 90 days or more — especially in areas with excess inventory or limited buyer demand. For real estate investors, this means accurate pricing and strong local market knowledge are more important than ever.

Move-in-ready, energy-efficient homes near good schools and public transportation are in high demand. As more employees return to the office, proximity to metro hubs and commuter routes has become a deciding factor for buyers — and a key metric for investors sourcing rental or fix and flip opportunities.

Rates are hovering around 6.5%, which is motivating move-up buyers to list and creating new opportunities for investors to purchase well-located properties. First-time buyers, especially in Maryland and Pennsylvania, are using down payment assistance programs to enter the market, keeping demand steady in affordable segments.

The real estate market in early 2025 is more balanced than it’s been in years. Homes that are priced right and in good condition are still attracting multiple offers, but the days of runaway bidding are behind us. For investors, this shift means a steadier, more predictable environment — one where strategy and timing matter more than speed. All signs point to a solid spring and summer ahead.

Not all deals are created equal — so how do you know if yours is worth it?

Look out for these key signs:

Pro Tip: The best investors don’t just crunch numbers — they ask smart questions and lean on their lender for guidance.

Learn the Right Questions to Ask →

The Washington, D.C. real estate market is expected to see roughly an 8% increase in home sales this spring, driven by a shift back to in-person work and renewed buyer and seller activity.

However, inventory is projected to remain below pre-pandemic levels, potentially keeping prices elevated or even flat.

While forecasts suggest more transactions, early data shows stable listing numbers, with February 2025 inventory nearly identical to the same time last year.

Success in today’s DMV real estate market requires smart strategy, not just capital. Use these insider tips to stay competitive and maximize your returns: